이 기사는 해외 석학 기고글 플랫폼 '헤럴드 인사이트 컬렉션'에 게재된 기사입니다.

2008년 리먼브러더스 파산으로 세계 금융 시스템이 혼란에 빠지면서 금융위기의 심각성을 확인한 뒤로 거의 15년이 흘렀다.

당시 어린아이였던 나의 학생들은 그 격변의 시대를 기억하지 못한다. 세계 금융위기, 더 정확하게는 북대서양 위기는 이제 역사책에 나올 만큼 옛날 일이 됐다.

그러나 그 여파는 여전히 남아 있다. 2010년대 초 유로존 위기 및 2020~2021년 팬데믹과 지난해 러시아의 우크라이나 침공이 글로벌 경제에 가져온 두 번의 큰 충격으로 심지어 여파가 강화되고 있다.

15년간의 혼란을 통해 이미 겪어왔기에 IMF(국제통화기금) 등의 주요 경제 전망이 모두 ‘향후 몇 년간 GDP(국내총생산) 성장이 부진할 것’이라고 예측하는 건 놀랍지 않다. OECD(경제협력개발기구) 회원국 대부분은 2008년 이래로 생산성이 약간 향상되거나 아예 향상되지 않았다. 한국의 생산성은 1990년대의 급속한 성장 이후 다른 선진국보다 낮은 수준에서 정체 중이다.

저명한 경제학자 폴 크루그먼은 “생산성이 전부는 아니지만 장기적으로 보면 거의 전부에 가깝다”고 말했다. 이는 한 사회가 얼마나 효과적으로 가용 자원을 사용해 소비자에게 가치 있는 산출물을 생산해내느냐에 대한 척도로서 생산성은 생활 수준을 결정하는 근본적인 요인이기 때문이다.

생산성이 향상되지 않으면 생활 수준이 정체된다. 이는 다시 여러 정치적인 결과로 이어진다. 일부 학자는 바로 이 때문에 전 세계적으로 포퓰리즘이나 다른 유형의 정치적 불안정이 급증하고 있는 것이라고 주장하기도 한다.

생산성의 개념은 종종 사람들이 더 열심히 일해야 한다는 뜻으로 오해되기도 하지만 사실 그렇지 않다.

건설노동자는 땅을 삽으로 더 빨리 파는 것보다 굴착기를 사용함으로써 생산성을 높일 수 있다. 생산성의 원동력은 혁신이고, 기계 등의 자본설비를 개발 혹은 개선하거나 생산을 조직하는 방식을 개선하는 것이다. 그래핀 등의 신소재나 더 정교한 공작기계, 머신러닝 시스템 등을 새롭게 발명하거나 린 생산(lean production·인력, 생산설비 등 생산능력을 필요한 만큼만 유지하면서 생산효율을 극대화하는 생산 시스템), 디지털 플랫폼 등의 새로운 프로세스나 비즈니스 모델을 채택하는 게 생산성을 높이는 주요 동인의 예가 될 것이다. 그런데 이 모든 건 다 투자가 필요하다.

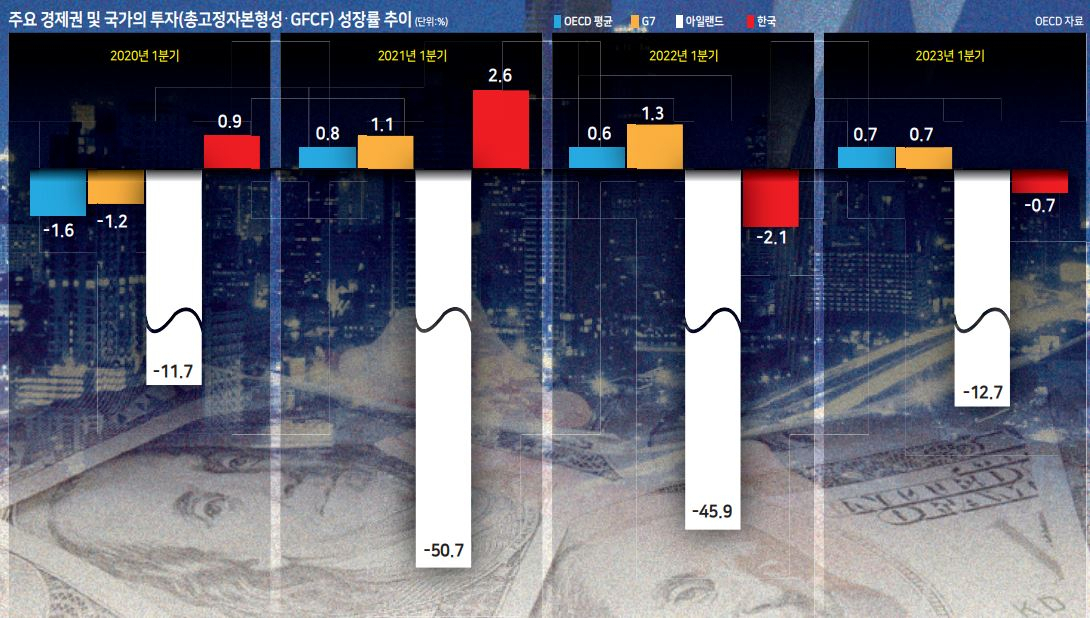

투자는 시간의 경과에 따라 변동성이 있지만 장기적인 추세를 보면 OECD 국가들에서 (특히 한국의 경우엔 두드러지게) 투자가 감소해왔다는 점은 분명하다. 잇달아 발생했던 위기들을 생각해보면 그다지 놀라운 일은 아니다.

글로벌 금융 시스템 내 높은 레버리지 비율로 2008년 금융위기는 매우 심각했다. 또 팬데믹 이후 많은 국가가 높은 정부 부채 비율로 어려움을 겪고 있다. 인플레이션(물가상승)이 부채의 실질 가치를 하락시키겠지만 그동안 더 높은 이자를 지불해야 한다. IMF에 따르면, 저소득 국가 대다수가 부채 곤경에 처해 있다. 이로 인해 인프라 유지 및 개선을 포함한 공공투자는 계속해서 부진을 면치 못했다.

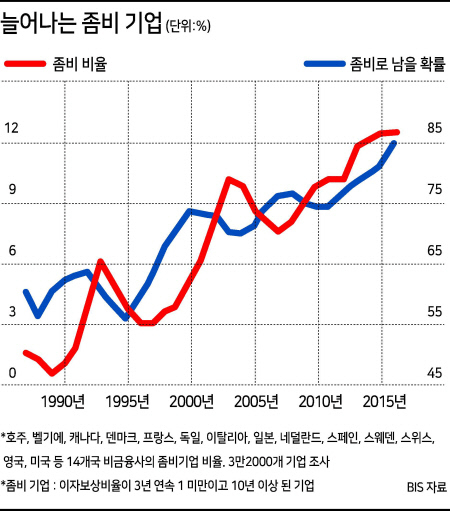

민간투자를 보면 잇단 위기로 인해 부채비율이 매우 높지만 부실 채권 인식을 원치 않는 대출기관들 탓에 운영이 계속되고 있는 ‘좀비 기업’이 증가했다. 친환경에너지, 전기차, AI(인공지능) 및 바이오 의학 등의 영역에서 흥미로운 혁신이 일어나고 있는 것은 사실이지만 그럼에도 수요의 부진한 성장은 투자를 위축시킬 것이다.

설상가상으로 우리가 의식하지 못한 부채의 존재 때문에 모든 국가는 공식 통계보다 상황이 더 좋지 않다.

이러한 부채 중 가장 중요한 건 ‘자연에 대한 부채’다. 경제활동은 사용에 대한 대가를 지불하지 않은 채 막대한 규모로 천연자원을 고갈시켜 왔다. 이는 불안정한 글로벌 기후, 생태계 붕괴, 안 좋은 공기, 작물 재배능력을 상실한 토양이라는 결과를 가져왔다.

이제 자연에 대한 추가적인 훼손을 줄이고, 불가피한 결과들에 적응하는 데에 다시 막대한 신규 투자가 필요할 것이다. 이 비용이 지금까지의 계산에 포함되지 않았다는 사실은 우리가 생각보다 더 가난하다는 것을 의미한다.

따라서 정책 입안자들은 시급히 투자에 집중해 생산성을 높여야 할 것이다. 이에 대해 어떤 이는 암울한 성장 전망과 높은 부채 부담으로 현재 투자할 여력이 있는 국가가 거의 없다고 반박할 수도 있다.

하지만 그렇다고 투자를 하지 않는다면 ‘자기실현적 저성장의 함정(self-fulfilling low growth trap)’에 빠지게 될 것이다. 부채 부담을 감당할 수 있는 수준으로 낮추면서 동시에 친환경에너지 발전이나 운송과 같은 필수 자산에 자금을 조달할, 가장 효과적인 방법은 성장을 통해 경제의 규모를 키우는 것이다.

또 하나 중요한 점은 ‘연간 성장과 더불어 국가의 재무제표도 모니터링해야 한다’는 것이다. 우리는 지금까지 현재의 소비에도 미래에 대한 투자와 동일한 가중치를 부여하는 GDP 성장에만 집중하며, 너무 오랫동안 우리 경제가 운용되는 방식이 지속 가능하다는 환상에 빠져 있었다.

올해 초 시작한 미국을 포함해 여러 국가가 인프라, 공장 등의 모든 전통적 자산뿐만 아니라 건강하고 교육 수준이 높은 인구라는 형태로 표현되는 인적 자본과 대기, 공기, 토양, 수질을 포함한 자연 자본까지 아우르는 ‘포괄적인 부(富)’에 대한 공식적인 통계를 개발하기 시작했다.

세계 경제를 짓누르는 여러 부채를 더는 늘리지 말고, 이제는 미래를 위한 좋은 관리인이 돼야 할 때다.

다이앤 코일 영국 케임브리지대 베넷 공공정책과 교수

Without investment, the economy will be stuck in a self-fulfilling low growth trap.

Diane Coyle

It is almost 15 years since the collapse of Lehman Brothers in 2008 confirmed the gravity of the crisis sending the world financial system into turmoil. My students were toddlers then and have no memory of that cataclysmic period. The Global Financial Crisis ― or more accurately the North Atlantic Crisis ― is old enough to be entering the history books.

Yet its consequences are still with us, reinforced by the Eurozone crisis in the early 2010s, and two subsequent huge shocks to the global economy: the pandemic in 2020-2021 and the Russian invasion of Ukraine in 2022. Spelled out as a decade and a half of tumult, it is not surprising that prominent economic forecasts (such as the IMF‘s) foresee only lacklustre GDP growth for the next few years. Most of the OECD member countries have experienced low or no productivity growth since 2008 (and South Korea’s productivity has levelled off below that of other advanced economies after growing rapidly in the 1990s).

The prominent economist Paul Krugman once said: “Productivity isn‘t everything, but in the long run, it’s almost everything.” This is because, as the measure of how effectively a society uses the resources available to it to produce and consumer valuable outputs, it is a fundamental determinant of living standards. If it does not grow, living standards stagnate. And that has political consequences: some scholars argue that this is the reason for a surge in populism or other types of political instability around the world.

Productivity is a concept often misunderstood as meaning people should work harder. Not so: a construction worker is made more productive by using a digger rather than by shovelling faster with a spade. The drivers of productivity are innovations, new and improved capital equipment such as machines, and improved ways of organising production. The invention of new materials such as graphene, sophisticated machine tools or machine learning systems, and new processes and business models such as lean production or digital platforms are examples of important productivity drivers. All require investment.

Investment is volatile over time. But looking at the longer term trends, it is clear that it has drifted downwards in the OECD economies (noticeably so in Korea). With the succession of crises, this is not surprising. The 2008 financial crisis was so serious because of the high level of leverage in the global financial system. Many countries have been struggling since the pandemic with high debt government burdens. Inflation will erode the real value of these burdens, but meanwhile higher interest payments have to be made; according to the IMF a majority of low income countries are in debt distress. So public investment ―including in maintaining and upgrading infrastructure ― has suffered.

When it comes to private investment, the succession of crises has led to a rise in the number of ‘zombie’ firms, highly indebted businesses invest but kept going by lenders who do not want to recognise bad debts. In any case, although there are exciting innovations in areas ranging from green energy and electric vehicles to AI and biomedicine, the prospect of slow growth in demand will discourage investment.

What‘s more, unacknowledged debts mean that every country is worse off than the official statistics show. Chief among these is the debt to nature. Economic activity has been depleting natural resources, without paying for their use, at vast scale. This has led to an unstable global climate, collapsing ecosystems, air that is harmful to breathe, and soil losing its capacity to grow crops. Mitigating further degradation of nature and adapting to the unavoidable consequences will require vast new investments. And the fact that the cost has not, until now, been counted means we are all poorer than we think.

So it is all the more urgent for policymakers to focus on investment and hence boost productivity. One reaction to this might be that with such dismal growth prospects and high debt burdens, few countries can afford to invest. But this would result in a self-fulfilling low growth trap. The most effective way to reduce the debt burden to affordable levels, and at the same time fund essential assets such as green energy generation or transport is to increase the size of the economy through growth.

Another key requirement is to monitor the economy‘s balance sheet as well as its annual growth. Through focusing only on GDP growth, which gives the same weight to consumption for today as to investment for the future, we have for too long been under the illusion that the way our economies operate is sustainable. More countries, including since earlier this year the United States, are starting to develop official statistics on comprehensive wealth ― all of the conventional assets such as infrastructure and factories, but also their human capital in the shape of a healthy and well-educated population, and their natural capital including the atmosphere and air, soil and water quality.

It is time to stop adding to the multiple debts weighing on the global economy, and start being good stewards for the future.