한국에 오면 가장 먼저 배우는 말 중 하나가 ‘고래 싸움에 새우 등 터진다’는 한국의 오래된 속담이다. 미국과 중국이 반도체 전쟁을 벌이고 있다. 반도체산업에 상당한 투자를 해온 한국이라는 작은 나라는 그들의 싸움에서 등이 터지지 않고 살아남을 수 있을까.

한국에 오면 가장 먼저 배우는 말 중 하나가 ‘고래 싸움에 새우 등 터진다’는 한국의 오래된 속담이다. 미국과 중국이 반도체 전쟁을 벌이고 있다. 반도체산업에 상당한 투자를 해온 한국이라는 작은 나라는 그들의 싸움에서 등이 터지지 않고 살아남을 수 있을까.이 문제에 답을 하려면 각 전투부대의 목표와 무기에 대해 명확히 알아야 한다. 미국의 무기, 더 정확히 말하자면 미국의 도구는 투자보조금과 수출 통제이고, 중국의 도구는 보조금과 지난 5월 중국 정부가 마이크론테크놀로지 제품 수입을 막은 것과 같은 수입 금지다.

도구의 성격이 무엇인지는 분명하지만 목표는 누구에게 묻느냐에 따라 달라진다. 미국의 어떤 정책입안자들은 투자보조금의 주요 목표가 양질의 일자리를 창출하기 위해 미국 내 칩 생산능력을 확대하는 것이라고 답할 것이다.

어떤 이들은 코로나19 당시 물류가 중단돼 태평양 지역에서 수입하던 칩이 부족해 자동차 제조업계가 어려움을 겪었던 것과 같은 공급망 교란을 피하는 것이라고 말할 것이고, 또 다른 이는 특히 중국과 대만에서의 수입을 최소화해 중국 정부의 통제로 인해 조임목(chokepoint)이 생기고, 미국 경제가 방해받을 가능성을 없애는 것이라고 할 것이다.

이 답변들은 메모리 칩, 주로 D램 칩과 낸드 칩 및 기존 로직 칩의 생산을 확대해야 한다는 주장이다. 이 칩들이 자동차와 소비자가전에 사용되는 칩들이기 때문이다. 위의 주장은 슈퍼컴퓨터나 인공지능(AI) 애플리케이션에 사용되는 최첨단 로직 칩의 생산을 확대해야 한다는 주장이 아니다. 최첨단 로직 칩 생산은 TSMC가 거의 독점하고 있고 일부는 삼성 파운드리에서도 생산된다(AI에도 일부 고급 메모리 칩이 필요하지만 매우 중요한 요소는 아니다).

한편 미국의 또 다른 정책입안자들에게는 반도체 전쟁의 목표가 21세기 경제적·군사적 전쟁터가 될 AI기술에서 중국의 발전을 늦추는 것이다. 이를 달성하기 위해서는 첨단 로직 칩 자체뿐 아니라 칩 설계에 대한 정보와 칩 제조에 필요한 포토리소그래피 및 기타 첨단 장비의 수출을 금지해야 하고 관련 생산능력에 대한 외국인 직접 투자도 금지해야 한다. 미국은 중국의 발전은 늦추면서 자국의 발전은 가속하기 위해 반도체 칩과 과학법(Chips and Science Act·일명 칩스법)을 통과시켜 반도체 연구·개발(R&D)에 공적 자금을 지원하기로 했다.

미국은 수출 통제와 R&D 보조금을 통해 첨단 로직 칩 분야에서 가능한 한 10년 동안 선두를 유지하고자 한다. 신기술 개발에서의 진척은 누적되는 것이기에 10년 후가 되면 AI 분야에서 중국에 대한 미국의 우위는 넘을 수 없는 벽이 돼 있을 것이다.

이러한 조치들이 의도한 효과를 가져올 것인가는 논란의 여지가 있다. 로직 칩 개발에서 중국은 미국에 크게 뒤처져 있다. 그러나 중국은 반도체 R&D에 상당한 추가 자원, 어떤 측면에서 보면 미국 정부가 동원하는 자원보다 더 많은 자원을 투입하면서 미국의 조치에 대응하고 있다. 선점 효과는 중요하지만 그게 전부는 아니다. 중국은 전기차를 비롯한 여러 산업에서 이미 미국을 따라잡았고 심지어 능가한 분야도 있다. 중국이 첨단 반도체에서도 그럴 것이란 가능성을 무시하는 것은 신중하지 못한 처사다.

미국이 중국의 발전을 늦출 수 있느냐는 미국이 다른 국가들의 협조를 구할 수 있느냐에 따라 크게 달라질 것이다.

첨단 포토리소그래피 장비는 네덜란드와 일본이 독점하고 있다. 예를 들어 만약 최고의 극자외선 리소그래피 장비를 구하고자 한다면 이 장비는 네덜란드 기업인 ASML에서만 구할 수 있다. 따라서 올해 초 미국이 네덜란드 및 일본 정부와 수출 통제에 동의하는 협정을 체결한 것은 매우 중요한 의미를 지닌다.

이런 상황이 한국에 시사하는 바는 무엇일까. 한국 기업들은 칩스법의 보조금을 활용해 미국 내 반도체 생산을 확장할 수 있다. 삼성은 이 법안 이전에 이미 텍사스주 테일러시에 새로운 반도체공장을 건설하겠다는 의사를 밝힌 바 있다. 그렇게 되면 삼성은 미국 기업인 인텔이나 글로벌파운드리와 동일한 조건으로 미국 시장에 지속해서 접근할 수 있다.

그러나 칩스법의 조항에 따라 지원을 받으면 삼성은 미국 정부와 이익을 공유해야 할 의무 또한 생길 수 있다. 게다가 이 법에 따르면 보조금을 받는 기업은 운영에 관한 자세한 정보를 공유해야 한다.

다른 조건이 동일하다면 한국의 지도자들은 삼성과 그 경쟁사인 SK하이닉스가 국내 제조업과 일자리에 투자하기를 바랄 것이다. 이를 위해 한국은 신규 공장 건설 승인 절차를 가속화하고 향후 관련 투자에 대해 세액공제를 확대하며 기술전문학교 수를 늘리는 ‘한국판 칩스법’을 통과시켰다. 그러나 이 법안의 내용은 국제적인 보조금 전쟁의 기준에 비하면 그다지 대단한 수준은 아니다.

어찌 됐든 삼성과 SK하이닉스는 이미 많은 칩을 해외, 특히 중국에서 생산하고 있다. 게다가 해외 생산 문제가 이들의 R&D, 즉 이미 오래전 유용성이 입증된 ‘팹리스(fabless) 모델’을 지연시킬 필요는 없다.

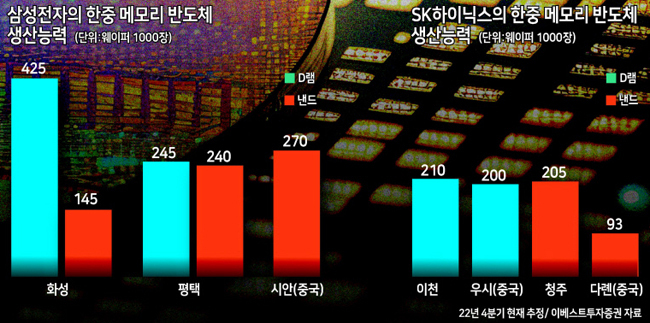

한국 기업들이 이미 중국에 많은 투자를 했다는 점을 생각해보면 그들의 딜레마를 알 수 있다. 미국 기업들이 중국 사업을 다른 사업에서 분리하거나 이것이 가능하지 않은 경우 중국 사업을 축소하고 있는 반면 한국 기업들은 양국 모두에서 사업하기 원한다. SK하이닉스 D램 칩 생산량의 절반과 삼성의 낸드 칩 생산량의 40%가 중국에서 생산된다는 점이 이들의 상황을 잘 보여준다.

마이크론 제품이 중국에서 금지된 것은 삼성과 SK하이닉스, 이 두 한국 기업에는 중국 시장 점유율을 높일 기회이기도 하다. 하지만 공격적으로 움직일 경우 조 바이든 미국 정부의 분노를 살 수 있기에 조심스럽게 움직일 것으로 예상된다.

그러나 한국 반도체업체들로서는 제조 장비를 중국 생산시설로 수출하지 않고서는 중국 사업을 유지할 수 없다. 이전 장비는 낡았고, 신규 교체 장비에는 신기술이 들어가 있다. 삼성과 SK하이닉스는 중국에서 주로 메모리 칩을 생산하기에 이 장비가 미국의 수출 규제에서 면제되기를 바라고 있을 것이다. 이 바람을 증명하듯이 이 두 기업은 중국 공장에 관련 장비를 계속 수출할 수 있도록 미국으로부터 한시적 유예를 받았다. 하지만 이 유예 조치를 연장해야 할 필요가 있으므로 한국 기업들은 중국 사업을 확장할 때 신중히 움직여야 할 것이다.

또한 삼성과 SK하이닉스는 최첨단 AI 관련 칩 생산시장에도 진입하고 싶어한다. 메모리 칩이 이미 상용화된 점을 고려했을 때 미래의 수익창출원은 고급 로직 칩이 될 것이다.

한국 기업들이 성공적으로 이 방향으로 움직인다면 결국 미국 및 중국 정부와 충돌하게 될 것이다. 미국은 네덜란드나 일본 기업들처럼 첨단 기술을 중국에 수출하지 말라고 요구할 것이고, 중국 정부는 아마도 분노해 삼성과 SK하이닉스가 중국 생산설비를 재정비하지 못하게 하거나 수익성 있는 중국 시장에 접근하지 못하게 함으로써 보복할 것이다. 그때가 되면 한국 기업들은 미국과 중국 중 하나를 선택해야 할 것이다.

지금까지 한국은 미-중 간 무역 및 기술전쟁 속을 잘 헤쳐 왔다. 두 고래 사이를 잘 헤엄쳐가며 부수적인 피해를 보지 않았고, 삼성과 SK하이닉스도 그럴 수 있었다. 그러나 이 평온한 바다의 시대는 곧 끝날지도 모른다.

Korea Amidst the Chip Wars

Barry Eichengreen

One of the first things a visitor to South Korea learns is the old adage about how, when the whales fight, the shrimp’s back is broken. The United States and China are fighting over semiconductors. The question is whether Korea, a smaller economy with considerable investment in the semiconductor industry, can survive their fight intact.

Answering this question requires clarity on the objectives of the combatants and their weapons. In the U.S. case, the weapons, or more precisely the instruments, are investment subsidies and export controls. For China they are subsidies and import bans, such as the ban imposed by Beijing in May on imports of the products of Micron Technology.

While there is clarity on the nature of the instruments, the nature of the objectives depends on who you ask. For some U.S. policy makers, the prime objective of the investment subsidies is to expand chip manufacturing capacity in the United States, with the goal of creating good jobs.

For others the objective is to avoid disturbances to supply chains like those during COVID-19, when logistics were disrupted and motor vehicle production suffered from shortages of chips imported across the Pacific. For still others, the goal is to minimize U.S. imports from China and Taiwan specifically, which Beijing could restrict, creating a chokepoint and disabling the U.S. economy.

These are arguments for expanding the production of memory chips, mainly dynamic random access memory (DRAM) chips and total flash memory (NAND) chips, and last-generation logic chips, since these are the chips used in motor vehicles and consumer electronics. They are not arguments for expanding the production of cutting-edge logic chips used in supercomputing and artificial intelligence (AI) applications, which are produced almost exclusively by Taiwan Semiconductor and, in some cases, Samsung Foundry. (Some high-end memory are also needed for AI, but they are not the critical element.)

For still other U.S. policy makers, the goal of the chip war is to slow China’s progress in AI, the technology on which 21st century economic and military battlefields will turn. Achieving this involves banning exports of cutting-edge logic chips, information about the design of such chips, photolithographic and other advanced equipment needed to manufacture them, and foreign direct investment in the relevant manufacturing capacity. To accelerate progress in the U.S. even while slowing it in China, the U.S. CHIPS and Science Act provides public funds for semiconductor research and development.

These export bans and R&D subsidies are intended to sustain America’s lead in cutting-edge logic chips, hopefully for as long as ten years. Since progress in developing new technology is cumulative, the country’s lead over China in AI will then be insurmountable.

Whether these measures will have their intended effect is debatable. China is significantly behind the U.S. in the development of logic chips. But it is responding to U.S. measures by throwing very considerable additional resources at semiconductor R&D – even more, by some measures, than are being mobilized by the U.S. government. First-mover advantage is one thing, but it is not everything. China has caught up and even surpassed the U.S. in other industries, such as electric vehicles. It would be reckless to dismiss the possibility that it might do likewise in advanced semiconductors.

U.S. success at slowing China’s progress will be heavily influenced by its success at enlisting foreign partners. Advanced photolithographic equipment comes exclusively from the Netherlands and Japan. If you want the very best extreme ultraviolet lithography machines, you can get them only from the Dutch company ASML. It was critical, therefore, that earlier this year the U.S. sealed a deal with the Netherlands and Japan in which their governments agreed to export controls.

So where does this leave South Korea? Korean companies can take advantage of the subsidies of the CHIPS Act to expand semiconductor production in the United States. Samsung had already announced the intention of building additional chip-making capacity in Taylor, Texas, prior to the act. This would ensure the company’s continued access to the U.S. market on the same terms as American companies Intel and GlobalFoundry.

But accepting aid under the provisions of the CHIPS Act may also oblige Samsung to share its profits with the U.S. government. In addition, the act obliges recipients to share detailed information on their operations.

Other things equal, Korean leaders would prefer to see Samsung and its rival, SK Hynix, invest in manufacturing and jobs at home. To this end, South Korea has passed its own version of the Chips Act, expediting the approval process for the construction of new factories, prospectively providing tax credits for such investments, and increasing the number of schools specializing in technology. But these initiatives are modest by the standards of the international subsidy wars.

In any case, Samsung and Hynix already do much of their chip production abroad, not least in China. Moreover, manufacturing abroad need not slow the progress of their R&D, the “fabless model” of production having long since proven its utility.

This last observation, that Korean firms are heavily invested in China, points up the dilemma. Whereas U.S. companies are separating their Chinese and other operations where they can, and curtailing their Chinese operations where they cannot, Korean companies have an interest in operating in both countries. That China accounts for half of Hynix’s production of DRAM chips and 40 percent of Samsung’s NAND chips tells the tale.

With the ban on Micron’s products, the two companies stand to expand their shares of the Chinese market. One can expect them to do so cautiously, given that moving aggressively would attract the ire of the Biden Administration.

But Korean chip makers can’t maintain operations in China without exporting manufacturing equipment to their facilities there. Old equipment is worn out, and replacement equipment embodies new technology. Since Samsung and Hynix produce mainly memory chips in China, they can hope that this equipment will be exempt from U.S. export controls. Affirming this hope, the two companies obtained waivers from the U.S. to continue exporting such equipment to their Chinese plants until October. The need to renew those waivers is yet another reason why they will move gingerly when expanding Chinese operations.

Moreover, the two Korean semiconductor giants aspire to move up-market into the production of leading-edge AI-relevant chips. OpenAI’s CEO Sam Altman encouraged them to do so on a visit to Seoul last month. High-end logic chips are the profit center of the future, given the commodification of memory chips.

And if Korean companies successfully move in this direction, they will come into conflict with the U.S. and Chinese governments. The U.S. will insist that they, like Dutch and Japanese companies, restrict their export of their advanced technologies to China. The Chinese government, predictably angered, will retaliate by prohibiting Samsung and Hynix from reequipping their Chinese facilities and exploiting the lucrative Chinese market. At that point, the Korean companies will have to choose between the U.S. and China.

So far, South Korea has been able to navigate the U.S.-China trade and technology war. It has swum between the two whales without becoming collateral damage. Samsung and Hynix have been able to do likewise. But this era of placid seas may coming to an end.