이 기사는 해외 석학 기고글 플랫폼 '헤럴드 인사이트 컬렉션'에 게재된 기사입니다.

미국을 포함한 주요 7개국(G7) 정상이 러시아중앙은행에 제재를 가하고 서방 금융기관이 러시아와 거래하는 것을 금지하기로 결정했을 때 글로벌 통화·금융질서에 막대한 변화가 있을 것이라 경고한 이들이 많았다. 이러한 제재가 다른 국가들에 금융을 ‘무기화’하려는 미국의 시도로 보일 수 있고, 언젠가 자신도 미국 제재의 대상이 될 수 있다고 생각한 정부와 중앙은행들이 달러화 및 미국 은행, 미국이 주도하는 국제은행간통신협회(SWIFT) 시스템에 대한 의존도를 낮추려고 할 수 있다는 것이다.

더 나아가 이 변화의 주요 수혜자는 중국이 될 것으로 예상했다. 지금까지 중국은 러시아와 서방 간 분쟁에 개입하지 않으려고 하고 있다. 블라디미르 푸틴 러시아 대통령과 시진핑 중국 주석이 양국의 우정을 재확인하는 와중에도 중국은 최근에 있었던 시 주석의 모스크바 국빈방문 당시 우크라이나 전쟁에 사용할 무기를 러시아에 지원하는 것을 꺼리는 모습을 보였다. 러시아-우크라이나 전쟁과 관련해 중국은 지금까지 금융적 제재를 가하지도 않았고, 받은 적도 없다.

따라서 달러 의존도를 낮추려는 국가엔 중국이 대안이 될 수 있다. 중국은 거대한 은행 시스템을 갖고 있고, 위안화 결제 원활화를 위해 페드와이어(Fedwire·미국 연방준비제도와 시중은행 간 지급 결제 시스템)와 미국이 운영하는 달러 결제망인 칩스(CHIPS)의 대안이 될 수 있는 위안화 국제 결제 시스템(CIPS)을 구축했으며, 중국 외 국가들이 중국 시스템 사용을 고려할 가능성도 꽤 있다.

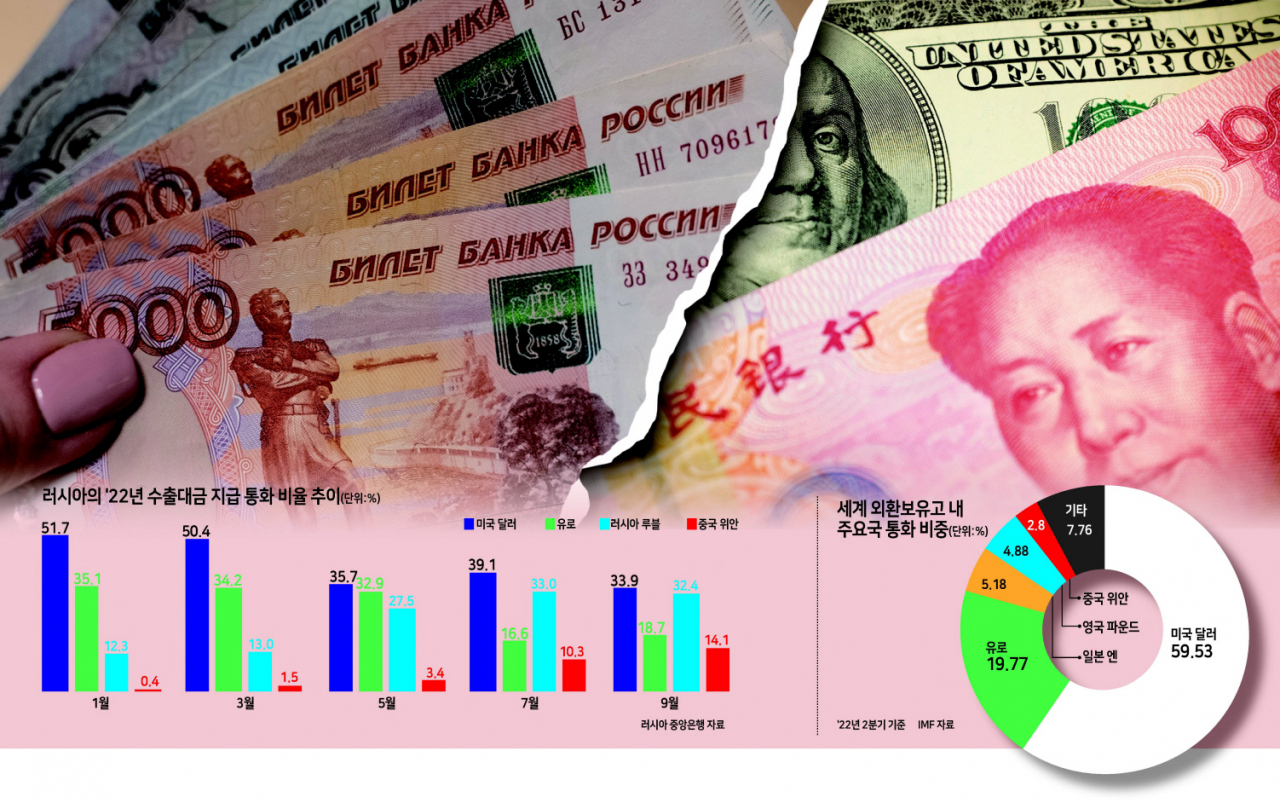

적절한 예로 더는 서방 금융 시스템에 접근할 수 없는 러시아를 들 수 있다. 러시아는 이미 수출대금의 14%를 위안화로 받고 있고, 지난해 러시아 기업들은 70억달러 규모의 위안화 표시 채권을 발행했다. 러시아 국부펀드는 약 450억달러어치의 위안화 표시 증권과 예금을 보유하고 있는데, 이는 펀드 총 자산의 약 30%에 해당한다. 러시아중앙은행이 마지막으로 외환보유액 포트폴리오 구성을 보고했던 2022년 1월 기준 러시아중앙은행 외환보유액에서 위안화가 차지하는 비중은 17%였다. 그때로부터 지금까지 러시아중앙은행은 달러와 유로를 팔 수 없었고, 또 금을 팔았다는 보고도 없으므로 현재의 외환보유액 포트폴리오 구성도 그때와 동일할 것으로 사료된다.

러시아의 상황을 생각해보면 이런 변화가 전혀 놀랍지 않다. 하지만 과연 다른 국가도 러시아와 같은 방향으로 움직일까. 지난해 말 시 주석이 사우디아라비아를 방문했을 때 사우디 측에 원유 수출대금을 위안화로 받을 것을 제안했고, 다른 여러 국가에도 비슷한 제안을 했다. 중국은 최근 파키스탄, 아르헨티나, 브라질 등의 국가와 위안화 청산 협정을 체결했고, 지난 3월에는 대(對)중국 무역에 위안화 결제를 허용할 것이라는 이라크중앙은행의 발표도 있었다.

그러나 사실상 사우디아라비아 같은 수출국은 위안화 허용 및 활용을 꺼리고 있다. 위안화가 여전히 달러만큼 자유롭게 전환 가능하지 않다는 것을 알고 있기 때문이다. 시 주석이 사우디아라비아 측에 수출대금 위안화 결제를 제안했을 수는 있지만 방문기간에 국제유가를 달러로 책정하는 관행을 바꾸는 것에 대한 진지한 논의는 이뤄지지 않았고, 또 사우디아라비아가 환율을 달러에 고정하는 오래된 관행을 버릴 수 있는지에 대한 논의도 없었다.

이런 상황을 봤을 때 많은 국가가 대중국 수출대금을 위안화로 받고 위안화를 널리 사용하게 될 것이란 예상은 그냥 예상으로 남을 것으로 보인다.

당연하게도 위안화로의 광범위한 이동은 데이터상에서도 보이지 않는다. 국제결제은행(BIS)에 따르면 무역 결제통화에 대한 접근이 이뤄지고 환 노출이 헤징되는 글로벌 외환시장의 거래량에서 위안화의 비중은 5%에 불과한 반면, 달러는 50% 정도를 차지한다. 또 SWIFT를 통해 이뤄지는 국가 간 결제 중 위안화가 차지하는 비중은 2% 미만이고, 국제통화기금(IMF)이 발표하는 세계 외환보유액 총액에서 위안화의 비중은 3% 미만이다.

물론 모든 국가가 외환보유액 통화 구성을 IMF에 보고하는 것은 아니다. 특히 제재에 대한 우려가 많은 국가는 보고를 하지 않을 가능성이 크고, 이런 국가의 은행은 SWIFT 전자 메시징 서비스를 이용하는 대신 e-메일이나 전화, 팩스 등과 같은 재래식 대안을 통해 해외 송금을 처리할 가능성도 크다.

러시아 같이 특수한 경우가 있긴 하지만 중국의 금융 중력엔 한계가 있을 것이라 판단할 만한 근거도 존재한다. 중국이 러시아에 전쟁물자를 지원해서는 안 된다는 미국의 경고는 중국이 결국 2차 제재의 대상이 될 수도 있다는 가능성을 제기하고, 그럴 경우 다른 국가의 은행과 기업이 중국 은행을 통해 대외 사업을 할 수 있는 여지는 거의 없을 것이다.

더욱이 중국 정부는 민간부문에 대한 태도를 거듭 바꿔왔다. 가장 악명 높은 예로 위챗, 알리바바와 같은 대형 IT 플랫폼에 대한 단속을 생각해보자. 중국 정부가 이렇게 IT기업에 대한 규제를 바꿀 수 있다면 금융회사에 대한 규제도 언제든지 바꿀 수 있을 것이다. 즉, 상하이에 준비통화를 보유한 외국 중앙은행에 대해, 또 중국의 국제 결제 시스템을 통해 자금을 이체하려는 상업은행에 대해 얼마든지 접근조건을 바꿀 수 있다는 것이다. 이러한 조치는 중국 정부의 자본 통제로 인해 가능하다. 시진핑의 중앙집권화된 권력은 그가 이러한 조치를 취하지 못하도록 막을 반대세력이 거의 없다는 것을 의미하기 때문이다.

아시아 및 기타 지역 국가들은 달걀을 중국이라는 바구니에 담기보다는 국가 간 결제에 현지 통화를 쓰는 것을 고려하고 있다. 싱가포르와 태국은 양국의 실시간 신속자금 이체 시스템인 페이나우(PayNow)와 프롬페이(Prompt Pay)를 연계했고, 참가 은행의 고객은 휴대전화 번호만으로 국외 송금을 수행할 수 있게 됐다.

말레이시아와 태국의 중앙은행은 링깃-바트 직접 결제 프레임워크를 확장함으로써 적격한 시중은행을 통할 경우 양국 간 직접 결제가 가능해졌다.

또 5개의 동남아 중앙은행은 국외 송금 시 달러나 위안화를 거칠 필요가 없도록 각국의 신속자금 이체 시스템을 연계하기로 합의했다. 인도네시아는 주요 20개국(G20) 의장국일 당시 이 방안을 더 확대하기 위해 어떤 규제개혁이 필요한지 식별하도록 ‘현지 통화 결제 태스크포스(Local Currency Settlement TF)’를 발족한 바 있다.

외환보유액 측면에서도 달러를 줄이려는 다각화 움직임은 위안화 중심이 아닌 한국 원화, 싱가포르 달러, 스웨덴 크로나, 노르웨이 크로네 및 뉴질랜드 달러를 늘리려는 다각화로 이어졌다.

오늘날 세계 외환보유액 중 미국 달러의 비중은 20년 전과 비교했을 때 약 70%에서 60%에 조금 미치지 못하는 수준으로 떨어졌는데 이 감소분의 4분의 1만이 위안화로 이동했고, 4분의 3은 소규모 국가에서 발행된 비전통적인 준비통화로 이동했다.

이러한 추세는 지정학적 요인보다 기술의 발전으로 인한 것이다. 페이나우나 프롬페이와 같은 결제 시스템은 디지털 네이티브 기술이기 때문에 연계가 쉬워 자금을 이체할 때 달러나 위안화를 거칠 필요가 없다.

또 자동 시장 조성 및 유동성 공급 알고리즘을 가진 디지털 외화 플랫폼의 부상으로 소규모 국가의 통화를 보유하는 것이 쉬워졌고 거래비용도 저렴해졌다. 그 결과, 소규모 국가의 통화가 결제 수단으로서, 또 대외 준비자산으로서 매력도가 커졌다.

많은 사람이 지정학적 요인들로 전 세계 통화·금융질서가 중국에 유리하게 재편될 것이라 추정했지만 최종 결정권은 기술의 손에 있을지 모른다. 만약 그렇다면 세계 질서가 매우 다른 양상으로 바뀔 수 있다.

배리 아이켄그린 미국 캘리포니아대 버클리캠퍼스 경제학과 교수

Geopolitics and the Future of the Global Monetary Order

Barry Eichengreen

When the United States and its G7 partners imposed sanctions on Russia’s central bank and barred Western financial institutions from doing business with Russian counterparties, multiple commentators warned of far-reaching changes in the global monetary and financial order. Other countries would see those sanctions as yet another step in America’s “weaponization” of finance. Governments and central banks, perceiving that they too might one day be on the receiving end of U.S. sanctions, would reduce their dependence on the dollar, U.S. banks, and the U.S.-dominated Society for Worldwide Interbank Financial Telecommunications (SWIFT).

China would be the principal beneficiary of these events, these predictions continued. So far, China has sought to remain above the fray in the dispute between Russia and the West. While Russian President Vladimir Putin and Chinese President Xi Jingping have reiterated their friendship, most recently on Xi’s high-profile trip to Moscow, Beijing has been reluctant to provide Russia with weaponry for use in its war on Ukraine. China has neither imposed financial sanctions on other countries in connection with the Russia-Ukraine war, nor has it been on the receiving end of such sanctions.

China therefore offers an alternative to countries seeking to reduce their dollar dependence. It has a large banking system. It has created a Cross-Border Interbank Payments System to facilitate renminbi settlement, and to provide an alternative to Fedwire and the Clearing House Interbank Payments System (CHIPS) through which dollar payments are made. Other countries are likely to consider making use of these facilities.

Russia, which no longer has access to the Western financial system, is a case in point. Russia already accepts the renminbi in payment for 14 percent of its exports. Last year Russian companies issued $7 billion of renminbi-denominated bonds. Russia’s sovereign wealth fund holds $45 billion of renminbi-denominated securities and deposits, some 30 percent of its total assets. Its central bank held 17 percent of its foreign exchange reserves in renminbi in January 2022, the last time it reported the composition of its reserve portfolio. Since the Bank of Russia has been unable to sell its dollars and euros between then and now, and since there are no reports of the bank selling gold, it is plausible that the composition of its reserve portfolio is the same today as it was then.

Given Russia’s circumstances, none of this will come as a surprise. But will other countries also move in this direction? When President Xi Jinping visited Saudi Arabia late last year, he suggested to his Saudi hosts that they should accept payment for their oil exports in renminbi. China has made similar suggestions to a range of other countries. China has recently concluded renminbi clearing arrangements with Pakistan, Argentina and Brazil among them. Last month, Iraq’s central bank announced a plan to allow renminbi settlement for the country’s trade with China.

In practice, however, exporters like Saudi Arabia remain reluctant to actually accept and utilize the renminbi. They are aware that China’s currency is still not freely convertible, unlike the dollar. President Xi may have suggested to his Saudi hosts that they should accept payment for their exports in renminbi, but there was no serious discussion during his visit of changing the convention that global oil prices should be quoted in dollars. There was no discussion of the possibility that Saudi Arabia might abandon its long-standing practice of pegging its exchange rate to the dollar. Evidently, much of this talk about other countries accepting payment for their exports to China in that country’s currency and of their using the renminbi more broadly remains just that, talk.

Unsurprisingly, a broad shift toward the renminbi is not visible in the data. According to the Bank for International Settlements, the renminbi accounts for only 5 percent of turnover in global foreign exchange markets, where currencies used in trade are accessed and currency exposures are hedged, whereas the dollar’s share is on the order of 50 percent. China’s currency accounts for less than 2 percent by value of all instructions for cross-border interbank payments sent through SWIFT. Per the International Monetary Fund, the renminbi’s share of global foreign exchange reserves remains less than 3 percent of the reported global total.

To be sure, not all countries report the currency composition of their foreign reserves to the IMF, and countries most worried about the possible imposition of sanctions are least likely to report. Their banks, instead of using SWIFT’s electronic messaging service, are also most likely to arrange cross-border transfers through old-school alternatives like email, telephone and fax.

But there is also reason to think, special cases like Russia notwithstanding, that China has limited gravitational pull financially. U.S. warnings that China must not help Russia with war materiel raise the possibility that Beijing could eventually become subject to secondary sanctions, in which case there will be little if any scope for banks and firms in other countries to do cross-border business via Chinese banks.

Moreover, China’s government has repeatedly changed its posture toward the private sector, most notoriously clamping down on the operations of large IT platforms like WeChat and Alibaba. If it can change the rules of the road for these IT firms, then it can also change the rules of the road for financial firms, including financial entities holding renminbi balances. This points to the possibility that it may, at some point, change terms of access for foreign central banks holding reserves in Shanghai and for commercial banks seeking to transfer funds through its cross-border payment system. China’s capital controls provide levers with which to make such changes. Xi’s centralization of power means that there are few countervailing forces to prevent him from taking such steps were he so inclined.

Rather than putting their eggs in China’s basket, other countries, in Asia and generally, have been looking to their local currencies for cross-border payments. Singapore and Thailand have connected their real-time fast payment systems, PayNow and PromptPay, enabling customers of participating banks to transfer funds between the two countries using just a mobile number. Bank Negara Malaysia and the Bank of Thailand have expanded their ringgit-baht direct settlement framework to enable Malaysians and Thais to make direct payments through qualified commercial banks. Five Southeast Asian central banks have signed an agreement to link their fast payment systems, bypassing the need to use either the dollar or the renminbi as a vehicle for cross-border transfers. Indonesia, during its G20 presidency, established a Local Currency Settlement Taskforce to identify regulatory reforms to further encourage the practice.

On the foreign-reserves front, similarly, diversification away from the dollar has not been diversification toward the renminbi, in the main, but rather diversification toward the Korean won, Singapore dollar, Swedish krona, Norwegian krone and New Zealand dollar. The U.S. dollar’s share of identified reserves has fallen from about 70 percent of the global total 20 years ago to a bit less than 60 percent today. Only a quarter of this fall has been matched by movement into the renminbi. Three quarters has been matched by movement into these nontraditional reserve currencies issued by smaller economies.

These trends reflect not so much geopolitics as developments in technology. Because payment systems like PayNow and PromptPay are digital natives, they are readily linked, removing the need to go through the dollar or renminbi when transferring funds. The currencies of these smaller countries have also become easier to hold and cheaper to trade with the rise of digital foreign-currency platforms featuring automated market-making and liquidity-provision algorithms. This in turn makes such currencies more attractive for payments and as a form of international reserves.

The presumption has been that geopolitics will reshape the global monetary and financial order in China’s favor. But technology may have the final say. And, if it does, it may alter that order in a very different way.